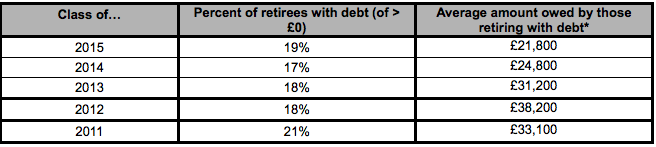

Almost one in five (19 per cent) of those planning to retire this year will do so with debts outstanding, averaging £21,800, according to new research from Prudential.

The insurer’s ‘Class of’ research into the future plans, finances and aspirations of those planning to retire in the next 12 months is now in its eighth year. This year’s results show that the ‘Class of 2015’ are more likely to retire in debt than those who gave up work last year – (17 per cent of those retiring in 2014 said they would have debts outstanding when they retired, compared with 19 per cent this year).

Prudential’s research has tracked retiree debt since 2011 and shows that despite some small fluctuations, the proportion of those retiring with debts outstanding has remained consistently around the one in five mark. There is a noticeable trend though that retirees’ average amount of debt has reduced over the years.

Those retiring with debts in 2015 say they will owe on average £16,400 less than those who retired in 2012 – representing an encouraging 43 per cent drop in the last three years (see table below).

The average ‘Class of 2015’ retiree with debts says that it will be just over three years before they are paid off – this also compares favourably with last year’s retirees who said it would take them four years. Meanwhile, almost one in 10 (nine per cent) of this year’s retirees with debts expect to take nine or more years to clear their debts, and a further five per cent believe they will never pay them off.

More than two in five (43 per cent) of this year’s retirees with debts have an outstanding mortgage – another figure that has remained stubbornly high since its peak at 52 per cent in 2011. Over a half (55 per cent) will have credit card debts.

On average, a female retiree with debts will owe £24,900 this year – up considerably since last year when the average owed was £20,700. Men retiring this year with debts will owe an average of £19,700, down significantly from last year’s £28,400.

The proportion of women expecting to be in debt when they retire is unchanged at 16 per cent, while the proportion of men who expect to have debts is slightly higher at 21 per cent compared with 19 per cent last year.

While the ‘Class of 2015’ have the highest expected annual retirement income for six years at £17,000 a year, debts remain a major drain on their finances. On average, debt repayments are currently costing them more than £200 a month, rising to over £500 a month for one in seven (14 per cent).

Stan Russell, a retirement expert at Prudential, said: “Our new research shows a welcome downward trend in the average amount of debt for people retiring this year. However, it is a concern that the proportion of people reaching the retirement milestone still owing money is refusing to fall.

For many, retirement is a time in life when it is necessary to re-assess household budgets, and any debts outstanding will inevitably make this job more difficult. A consultation with a financial adviser or retirement specialist can help people to get their finances ready for life after work.

“Debt does not have to be a major issue in retirement though, as long as people have a realistic repayment plan in place. Citizens Advice Bureaux can provide free help on managing and paying off debt, and the Pensions Advisory Service can help with retirement income planning and related issues.”

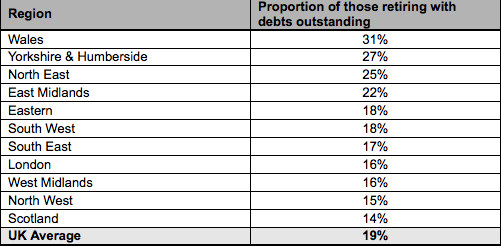

Regional breakdown

Retiring in debt

In response to the following question:

“Approximately how much personal debt do you think you will have at the point you retire?”